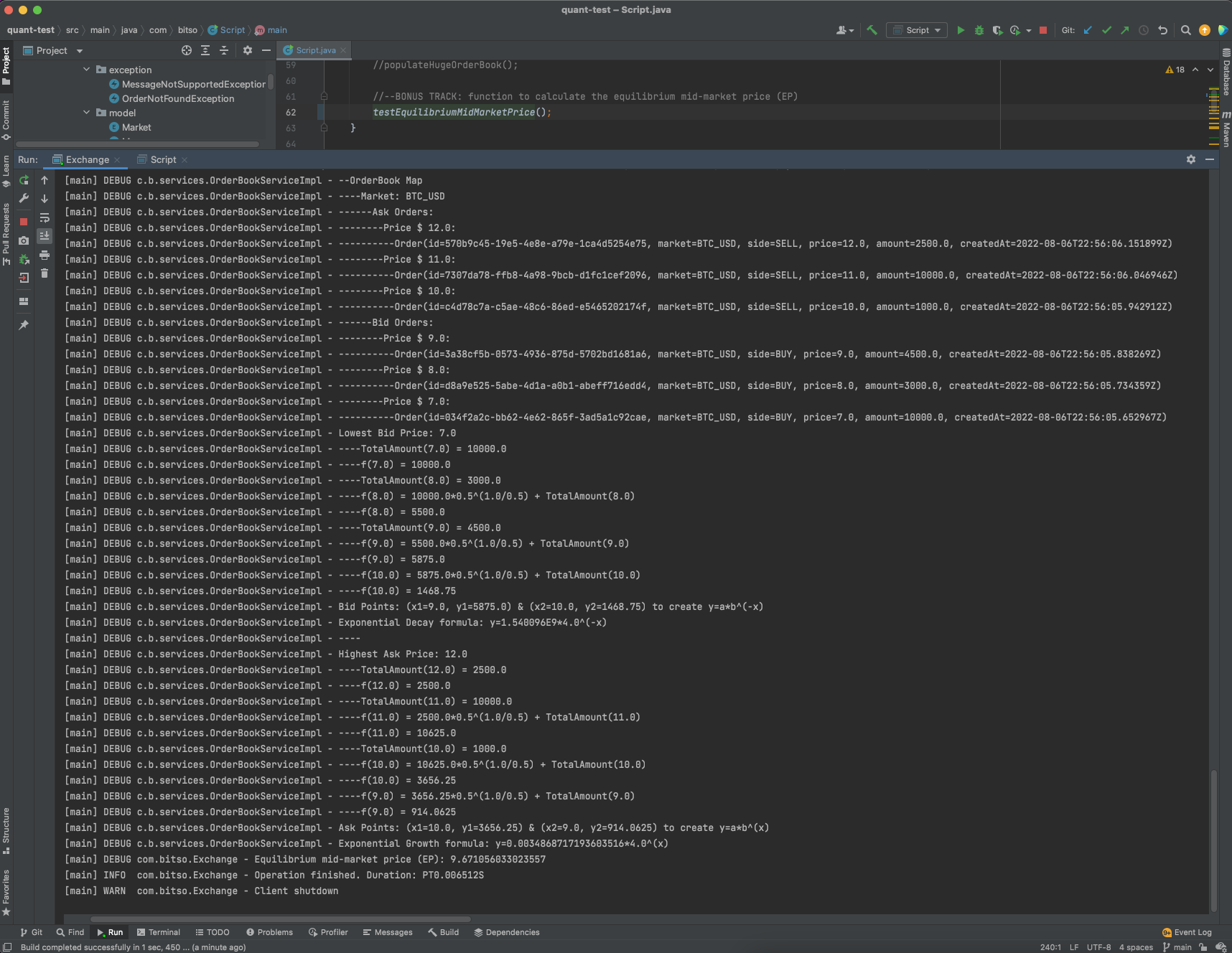

Note Bonus track included: function to calculate the equilibrium mid-market price (EP) which is the equilibrium price of cumulative discounted total volume functions of bid and ask side; given the parameter of half-life. See the last screenshot image.

The goal was created a simplistic framework of an exchange. I used Java NIO in order to have non-blocking I/O sockets.

- JDK 17

- Maven 3.8.6

The message is encoded in a similar way to how Financial Information eXchange (FIX) protocol works.

| Tag | Description | Values | Description |

|---|---|---|---|

| 0 | BeginString | BITSO | Constant value |

| 1 | MessageType | A,D,M, P | Add, Delete, Modify, Print |

| 2 | OrderSide | B,S | Buy, Sell |

| 3 | Price | e.g. 100.0 | Order Price |

| 4 | Amount | e.g. 72.0 | Order Volume |

| 5 | OrderId | e.g. 123e4567-e89b-12d3-a456-426614174000 | Unique UUID |

| 6 | Market | e.g. BTC_USD | Symbol Market |

Read more about FIX protocol: here

ADD Message

0=BITSO;1=A;2=B;3=23728.9;4=0.01;6=BTC_USDDELETE Message

0=BITSO;1=D;5=12300000-0000-0000-0000-000000000000MODIFY Message

0=BITSO;1=M;4=0.02;5=12300000-0000-0000-0000-000000000000PRINT Message

0=BITSO;1=P;6=BTC_USDClone the repository to any folder in your computer

git clone https://github.com/andresort28/quant-test.gitRun the following steps to take a complete test in order to populate an OrderBook and fully filled a trade:

- Start the

Exchangeserver just running themain()method of the Exchange class. - Uncomment only

populateOrderBook()in theScript.main()method and run. It will populateBTC/USDMarket with BUY and SELL Orders. - View the console logs in the

Exchangeterminal and select an Order in the OrderBook you want to fill. Take a look that the methodScript.executeTrade()will send a BUY Order (by default), so you can choose an Order to fill in theAsk Sideof the OrderBook and then, you can edit the variablespriceandamountinsideScript.executeTrade()method in order to fill those SELL Orders you want partially or completely. - Comment

populateOrderBook()and uncomment onlyexecuteTrade()andprintOrderBook()inScript.main()method and run. It will try to fill the new BUY Trade you send to the Exchange against the Order you choose above. It will also print the final OrderBook state. - View the console logs in the

Exchangeterminal to see the entire process.

The solution is guaranteeing thread-safe on all operations and still handle a time complexity of O(1) and O(logn) for the most operations with ConcurrentHashMap and PriorityBlockingQueue as non-blocking data structure for the OrderBooks.

O(1)at time to SEARCH an Order in the Orders Maps.Mapused to store Orders by its OrderId (UUID) as key.

O(1)at time to SEARCH the OrderBook where an Order is.Mapused to store OrderBooks by Markets as key.

O(1)at time to SEARCH the Orders in its respective OrderBook.Mapis used to store Order's Queues by Prices as key.

O(1)at time to SEARCH the highest priority Order in an OrderSide (Ask/Bid)Queueis used to store Orders using the creation date as the defined priority.

O(logn)at time to ADD a new Order in its respective OrderSide (Ask/Bid) in the OrderBook.Queueis used to store the Orders in (First-In First-Out) FIFO order, but in this case it is a PriorityBlockingQueue.

O(logn)(worst case) at time to DELETE an Order that is fully filled in the OrderBook.- Each OrderSide uses a

Queueso the.remove()method, remove the head of the Queue. - However, when an arbitrary Order needs to be removed from the OrderBook (Queue) it could take

O(n)in the worst case finding its index. - It only takes

0.025 msto search for an Order 2000 Orders with (CPU=IntelCorei9andRAM=16GB).

- Each OrderSide uses a

O(logn)(worst case) at time to MODIFY an Order that is partially filled in the OrderBook wherenis the total of Orders at the same Price.- Because OrderBook uses Queues, the Order must be first removed from the Queue arbitrarily, which implies the same time complexity of DELETE operation, and then it needs to be added again.

Note: Because this solution is just a prototype, it does not use any database neither any kind of indexing. However, if we used indexing it could reduce the time complexity of DELETE operation to O(1).

The Script contains the two following stress-tests:

-

Small stress-test:

- The method

populateSmallOrderBook()create5,000Orders in the OrderBook (500 orders for each of the 5 prices on each side). - It is only the 1,25% of the Huge stress-test, but it's faster to run to measure processing time.

- The following times we captured with this stress-test on a CPU Intel Core i9 and a RAM of 16GB:

- ADD Messages

-

Message Amount Orders filled Time ADD 10 1 0.000775s ADD 100 2 0.000951s ADD 500 15 0.001231s ADD 1000 21 0.001006s

-

- MODIFY Messages (by UUID)

-

Message Amount Bigger Amount Time MODIFY 39 40 0.0018s MODIFY 86 90 0.000753s MODIFY 27 30 0.000904s MODIFY 2 99 0.000611s

-

- MODIFY Messages (by UUID)

-

Message Amount Smaller Amount Time MODIFY 90 10 0.000831s MODIFY 3 1 0.000902s MODIFY 68 30 0.000743s MODIFY 71 2 0.000850S

-

- DELETE Messages (by UUID)

-

Message Time DELETE 0.000922s DELETE 0.000559s DELETE 0.000718s DELETE 0.000239s

-

- ADD Messages

- The method

-

Huge stress-test:

- The method

populateHugeOrderBook()create400,000Orders in the OrderBook (2000 orders for each of the 100 prices on each side). - However, since it takes so long to receive all 400,000 messages in the Exchange, you can stress the Exchange with

the

Small stress-testto verify the above results and make sure that it guaranteethread-safeon all operations and a time complexity ofO(1)andO(logn)in the all the operation in the OrderBook.

- The method

- The idea is to create a simplistic framework, that's why I did not use

Nettydirectly as the client-server framework, and I usedNIOinstead. - Any dependency injection framework is used, so I apply Singleton pattern for the repositories, services and server classes.

- I decided to use

Repository Patterninstead ofDAOto be able to scale the framework to use database like Redis with the current Repository layer - This is a prototype and does not implement an indexing database, so I stored duplicate objects

Order(In Orders Maps and OrderBook Maps) to guaranteeO(1)in search, add, update and delete operations. - On rare occasions, the

OrderBookis printed without showing all the items ordered by thecreatedAtfield. However, this is not a problem per se, rather thePriorityBlockingQueuemainly guaranteesFIFOwith the element in its head.

- We could use a database option like

kdb+oRedisto guarantee fast performance - We can use

Jedis(Possibly with JedisPool to be thread-safe), orLettuceorRedissonfor a better scalability as Redis library for Java - We could use a message broker like

kafkato support multiple orders from multiple symbols instead ofSocketChannels

- Run the Exchange

- Run the Script to send messages to the Exchange to populate an OrderBook (BTC_USD)

- Exchange receives the message and process each connection printing the Orders and OrderBook Maps

- Run the Script to send a new Buy Trade (price=400, amount=10) to the Exchange (To fill 2 Sell Orders at price=400)

- Exchange add the new Buy Order and the Matching Engine try to fill the new Trade with the 1st and 2nd Sell Orders (price=400) in the Ask Side with FIFO order

- Run the Script to send a new Print message to the Exchange

- Exchange prints the final OrderBook with the 1st Sell Order (price=400) with new amount of 50 (before 51)

- BONUS TRACK: The Script contains a method to run the test to populate the OrderBook with a sample case and calculate the equilibrium mid-market price (EP) which is the equilibrium price of cumulative discounted total volume functions of bid and ask side; given the parameter of half-life.

Copyright (c) 2022 Andres Ortiz.