>> EuroCRR(50,50,.05,1,.3,.01,100,1)

ans =

6.7936

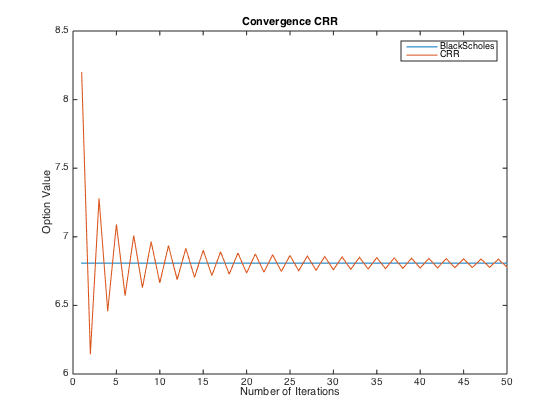

>> ConvergenceCRR(50,50,.05,1,.3,.01,50,1)

% Oscillates above and below.

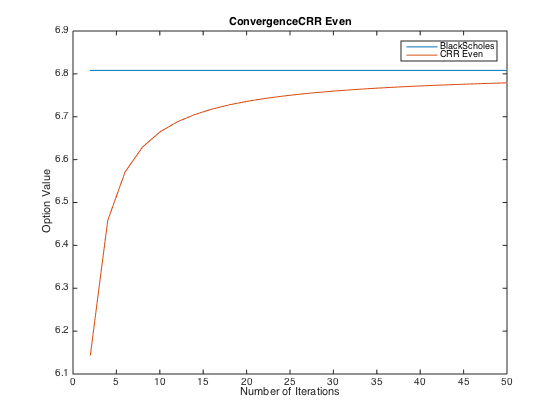

>> ConvergenceCRREven(50,50,.05,1,.3,.01,50,1)

%Converges smoothly from below.

{kind=link}

{kind=link}

{kind=link}

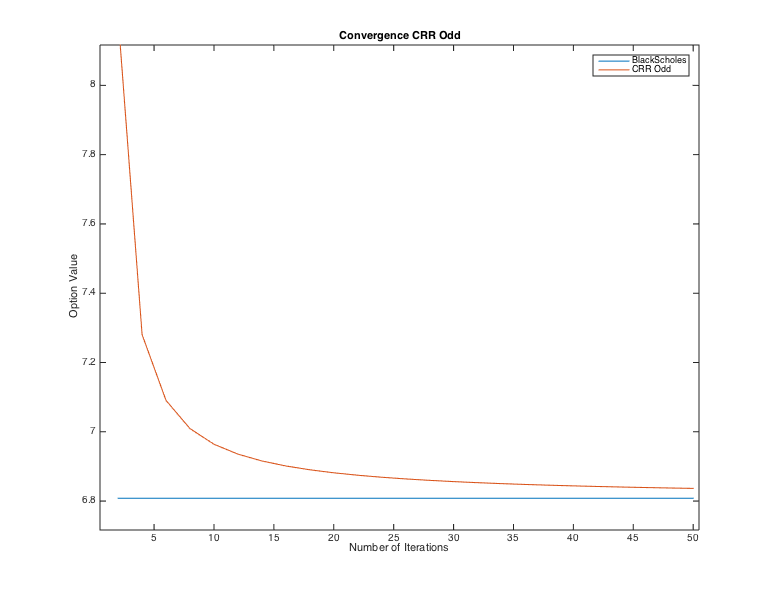

>> ConvergenceCRROdd(50,50,.05,1,.3,.01,50,1)

% Converges smoothly from above.

>> Binomial(50,47,.05,1,.3,.01,100,1,0,'EQP')

ans =

8.3236

>> Binomial(50,47,.05,1,.3,.01,100,1,0,'TIAN')

ans =

8.3186

>> Binomial(50,47,.05,1,.3,.01,100,1,0,'CRR')

ans =

8.3217

>> Binomial(50,47,.05,1,.3,.01,100,1,0,'LR')

ans =

8.3067

-

Brandimarte, Paolo. Numerical Methods in Finance and Economics: A MATLAB-based Introduction. Hoboken, NJ: Wiley Interscience, 2006. Print.

-

Haug, Espen, Gaarder. The Complete Guide to Option Pricing Formulas. New York, NY: McGraw-Hill, 2006. Print.