The course examines numerical methods for valuing financial derivatives. Topics include:

- Tree Methods

- Finite Difference Techniques

- Financial Engineering Methods and MATLAB

Asian option with geometric average:

>> GeoCall(30,30,.07,.01,.30,1)

ans =

2.2870

Asian option with geometric average:

Asian option with geometric average:

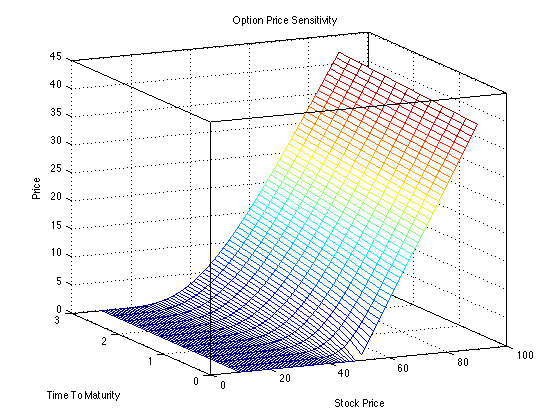

>> BlackScholes(50,50,1,.05,.2,0.02,1,0)

Price

ans =

4.6135

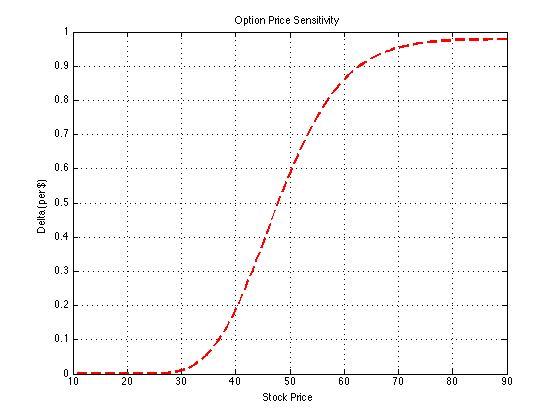

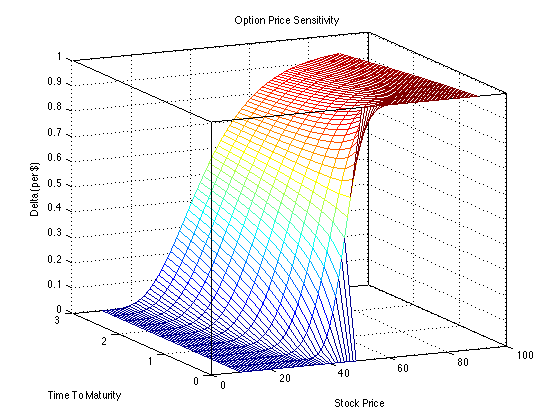

>> BlackScholes(50,50,1,.05,.2,0.02,1,1)

Delta

ans =

0.5869

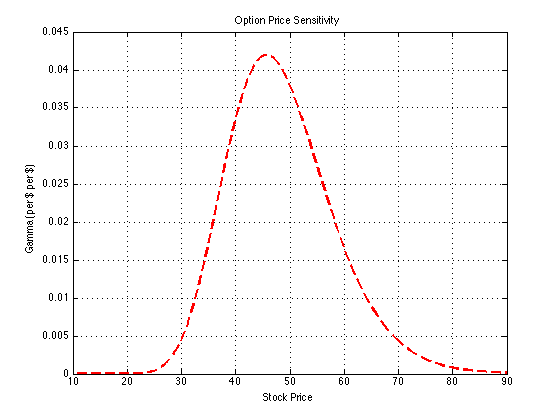

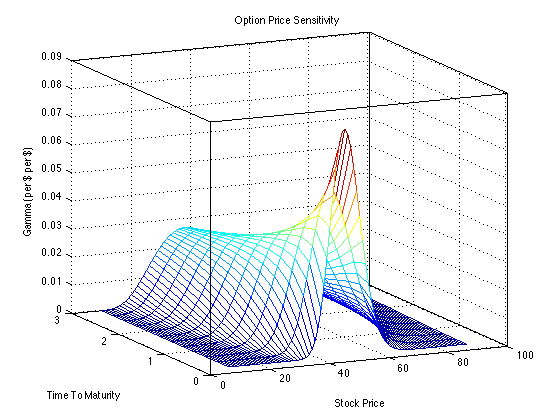

>> BlackScholes(50,50,1,.05,.2,0.02,1,2)

Gamma

ans =

0.0379

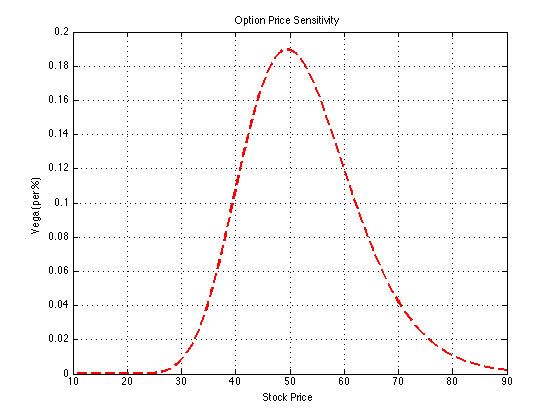

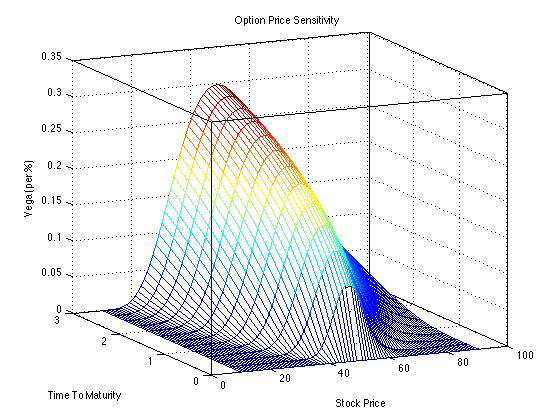

>> BlackScholes(50,50,1,.05,.2,0.02,1,3)

Vega

ans =

0.1895

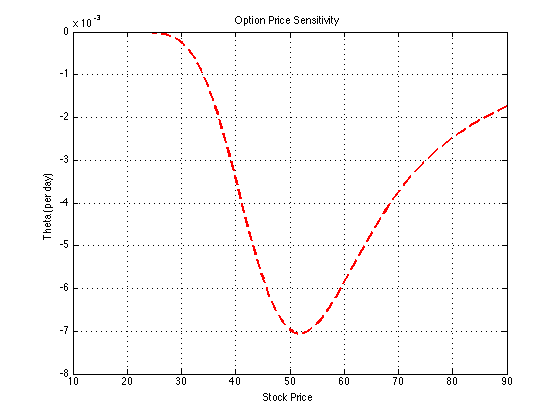

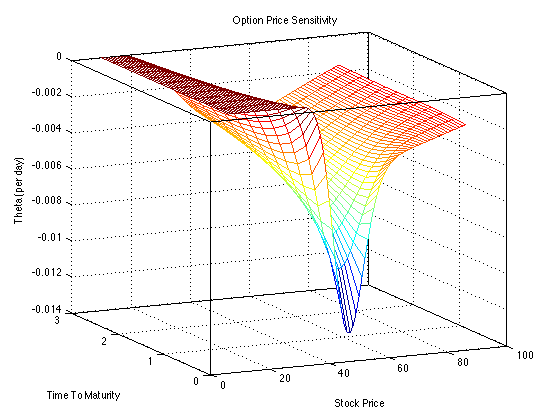

>> BlackScholes(50,50,1,.05,.2,0.02,1,4)

Theta

ans =

-0.0070

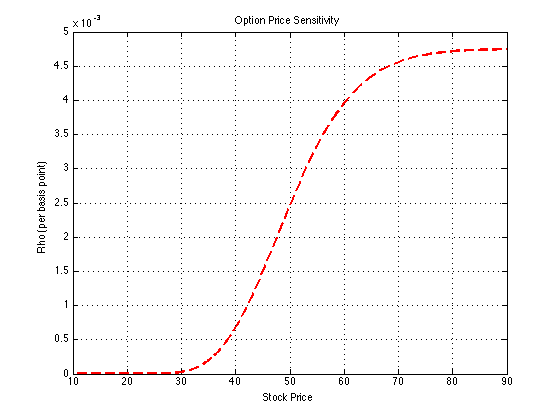

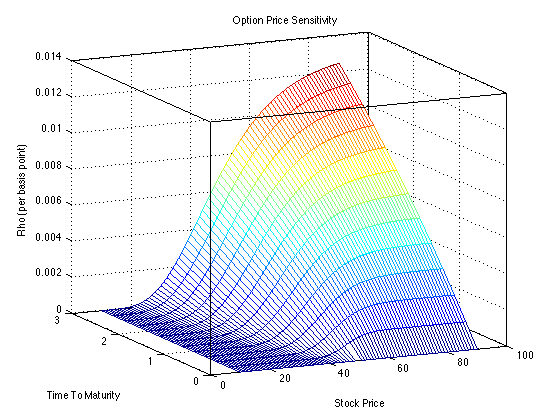

>> BlackScholes(50,50,1,.05,.2,0.02,1,5)

Rho

ans =

0.0025

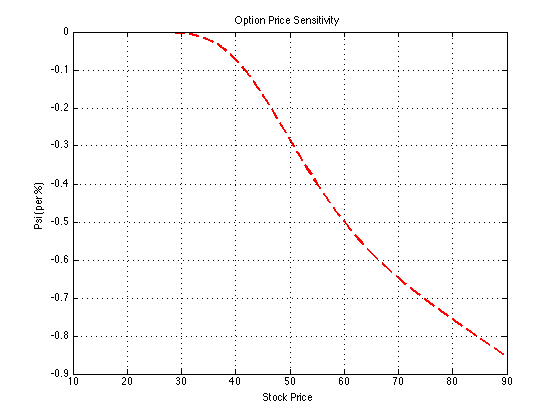

>> BlackScholes(50,50,1,.05,.2,0.02,1,6)

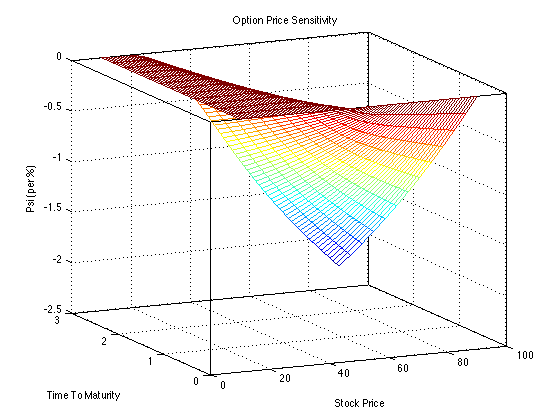

Psi

ans =

-0.2848

>> BlackScholes(50,50,1,.05,4.6135,0.02,1,7)

Implied Volatility

ans =

0.2000

>> BSImpliedVol_Newton(50,50,1,.05,4.6135,0.02,1)

Implied Volatility (Newton's Method)

ans =

0.2000

Write a function BSCall(S, K, r, q, vol, T) that returns the BlackScholes price of a call.

>> BSCall(50,50,.04,.017,.20,1);

4.4555

Write a function BSPut(S, K, r, q, vol, T) that returns the BlackScholes price of a put.

>> BSPut(50,50,.04,.017,.20,1);

3.3378

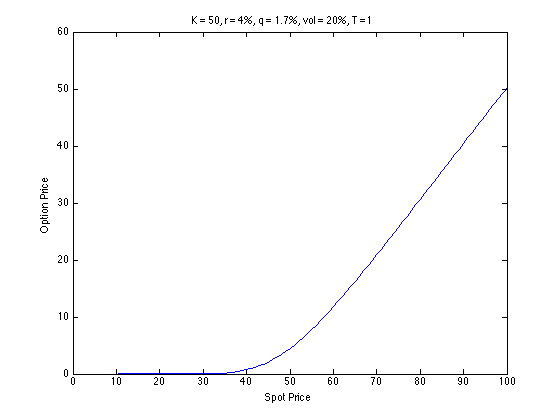

Write a script function that plots the price of a European call versus the Stock price S given K = 50, r = 4%, q = 1.7%, vol = 20%, T =1.