Revenue multiple is one of the most ubiquitous — and arguably crudest — metric used across Wall Street and Silicon Valley to value tech companies. If you were a fly-on-the-wall at your local mom-and-pop Hedge Fund or Venture Capital firm you’d likely hear in-depth conversations like:

- “It’s a piece of garbage but it’s trading under 1x revenue and cheap.”

- “This company is trading at 5x revenue?! That’s cheap!”

- “This company is trading at 5x revenue?! Short it.”

- “10x is not bad if you believe the addressable market and market share story.”

- “[XYZ] fund got in at 12x and they’re pretty smart. It’s trading at 6x now. Take a look at it.”

- “It’s priced at 100x but they’re purposely under monetizing. If you normalize things it’s cheap.”

- “It’s expensive using any metric but I think the founder will make us money.”

- “Where’s lunch? I thought you ordered an hour ago.”

If none of this makes sense to you, hopefully this brief primer on revenue multiple will make things a bit clearer. My hope is you gain a better understanding of revenue multiple and how (as a tech employee or entrepreneur) company decisions can potentially impact valuation. I’ve structured this README in a FAQ format so feel free to jump around.

- Revenue multiple is a popular valuation shortcut to quickly evaluate and value technology companies.

- It can also be viewed as a rating that scores a company’s long-term business prospects and popularity. (Read the race car analogy in the next section if you want a simplified conceptual explanation)

- More importantly revenue multiple can represent an expectation investors have on a business and can influence management decision making.

- Revenue multiple can be useful when comparing companies that have different levels of profits but similar business characteristics (i.e. competition, gross margins, addressable market, etc.)

- All revenue is not created equal and revenue multiple captures a complex balance of a company’s 1) growth prospects, 2) profitability, and 3) long-term risk profile.

- The key to using revenue multiple responsibly is to have a strong understanding of the underlying unit economics of the business being valued.

- Cash flow still matters long-term.

- The literal definition is enterprise value (market cap + debt — cash) divided by revenue.

- There are plenty of resources online if you need detailed definitions for enterprise value, valuation multiples, etc.

- Conceptually think of revenue multiple as a rating — or score — for a company’s long-term cash flow potential and general popularity.

What do I mean by rating? Imagine each business is a car in a race that has not yet started. Each car is unique with different top speed, fuel efficiency, tires, driver, crew, etc. Your goal is to pick the cars that will lead the pack and win the race. The race organizer, on the other hand, wants to arrange each car’s starting position so that everyone finishes around the same time.

So what does the race organizer do? They decide to use a rating system where the best and most popular cars start at the back and the less desirable cars are put at the front with a head start. In this rating system higher numbers go to the back and lower numbers move to the front. Picking a winner becomes trickier under these conditions, but the crowd can be noisy and ratings can be imperfect. You have your own rating system to rank the cars, but must now also account for the rating the organizer and crowd has given to each car to figure out which cars have the best odds of winning given their relative position. This is the essence of investing using revenue multiple.

- Revenue tends to be a much more stable value than using a tech company’s cash flow or profit number.

- Provides a quick snapshot of investor sentiment on the company and its business prospects without needing to make non-gaap accounting adjustments.

- Allows comparability of similar companies that may have much different (discretionary) operating structures.

- Many key decision makers cut their teeth using the metric and still use it out of habit and comfort level.

Many technology companies do not generate profits that reflect the true earnings potential of the underlying business and revenue multiple serves as an alternative metric to try and give a clearer view.

- I’ve seen investors use both but growth focused investors will favor applying a multiple on forecasted revenue while value (or cash flow) focused investors will use reported revenue.

For those evaluating high multiple companies, what’s important to remember is companies with high revenue multiples (i.e. 20x) today are assumed to see their multiple decline to rational levels over time. Using forecasted revenue requires an investor to think critically about the trajectory of a business, but allows them to apply a more reasonable multiple.

- Many tech companies have very large cash balances which can distort the Price-to-Sales ratio (which includes cash) and make it difficult to compare the business to other companies.

- For companies with high revenue multiples it can make a lot of sense to forecast cash flow to see if the current valuation can be justified using a reasonable and attainable multiple in the future.

- Building a DCF is a good way to test what an investor needs to believe in terms of total addressable market, market share, margins, and profitability to justify a high revenue multiple valuation.

- Revenue multiple can serve as a sanity check for cash flow based analysis (and vice versa).

- Although it is a revenue based metric, the revenue multiple the stock market applies does (attempt to) account for a company’s underlying expenses when looking under the hood.

- High margin, high growth companies tend to have a higher multiple when compared to lower margin, lower growth companies (all else being equal).

- If you believe valuation is ultimately a function of profitability and cash flow, revenue multiple can be estimated using the Gordon Growth Model.

- Also known as dividend discount model, Gordon Growth Model is a way to value a company based on the theory a business is worth the sum of all of its future dividend payments discounted back to their present value.

- The value or price (variable P) of a business is calculated by taking the value of next year’s dividend (variable D1) divided by a constant cost of capital (variable r) less a constant dividend growth rate (variable g) in perpetuity.

- Most tech companies do not pay out dividends, but the formula can be repurposed using estimated earnings or cash flow to calculate business value and ultimately revenue multiple.

- There are many resources online to learn how to derive various valuation multiples using the Gordon Growth Model but in general terms revenue multiple can be calculated:

Profit Margin × Profit Payout × (1 + g)/(r − g)

Most investors are primarily focused on growth rate (variable g) when evaluating revenue multiple, but business profitability (Profit Margin), management capital allocation decisions (Profit Margin, Profit Payout, variable r), and general market sentiment (variable r) are also drivers that impacts a company’s revenue multiple.

- There is a wide range of rule of thumbs investors and executives use to approximate multiple.

- One concept I have seen generally applied is (Growth rate % / 10) + 1 = Forward Revenue Multiple.

- The company being valued has stable growth, payout rate, and profitability. (Difficult assumptions to have for tech)

- For companies undergoing strong growth, a DCF or the multistage model may be used and/or more appropriate.

While imperfect the Gordon Growth Model provides a framework to gauge and understand market expectations for a company’s growth and returns. If a company is valued at a certain revenue multiple, we can use Gordon Growth to try and connect the dots to see what we need to believe in terms of growth and profits long-term to justify the multiple.

- Growth

- Recurring revenue

- Churn / Retention rate

- Gross margin

- Customer acquisition costs

- Customer lifetime value

- Profitability of an incremental new customer

- Addressable market size

- Bill Gurley provides an excellent overview of the key business characteristics that would be used to separate high quality revenue companies from low quality revenue companies, and therefore the traits that warrant high price/revenue multiples.

- Factors that drive long-term, sustainable profits will command premium revenue multiples.

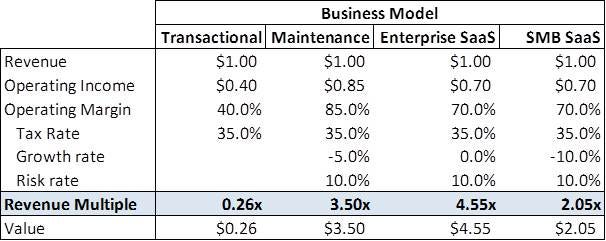

- Using Gordon Growth Model and applying generic tech business characteristics we can estimate what each type of revenue stream is worth in terms of a baseline revenue multiple

- Transactional businesses (i.e. one time sales, hardware, services) have substantially lower multiples while businesses with recurring revenues command higher multiples (all else being equal).

- Dave Kellogg has a thoughtful post walking through perpetual vs SaaS business models and how SaaS companies potentially fetches 1.8x the revenue multiple of perpetual companies because they are worth 1.8x the revenue multiple of perpetual companies.

- Keep in mind most companies have a mix of different types of revenue (one time, recurring, high margin software, low margin services) and a blended revenue multiple is required to value a company (i.e. 50% transactional, 50% recurring revenue blends to 3x “fair” multiple)

There are a lot of assumptions and moving parts here but the goal is not to come up with a precise value but to find a reasonable valuation baseline when evaluating a company. Most technology companies certainly trade at values in excess of these baseline values since this approach only captures the value of existing revenue streams and does not attempt to value new business prospects and other growth opportunities.

- 1x predominantly hardware or transactional revenue with little to no growth prospects. Typically lower margin products.

- < 3x will typically attract cash flow investors assuming the revenue includes significant recurring revenues.

- 3x to 5x is typically considered “fair” but interesting opportunities can be found if the market is underestimating growth opportunities.

-

10x companies are getting credit for revenue quality and growth prospects.

- Over time you will develop your own mental framework for what you consider is a reasonable revenue multiple.

Meandering between finance & software. Software Engineer. Former Tech Analyst at Relational Investors. Tweets tech, investing, JavaScript, shareholder activism.

Meandering between finance & software. Software Engineer. Former Tech Analyst at Relational Investors.