Statistical Arbitrage or StatArb “is a class of short-term financial trading strategies that employ mean reversion models involving broadly diversified portfolios of securities (hundreds to thousands) held for short periods of time (generally seconds to days). A pairs trade is a trading strategy that involves matching a long position with a short position in two stocks with a high correlation.

Within this project I explored the financial sector for any pairs available in the US market. I then created trading signals and the backtested the code to find the CAGR of the trades.

- Extracting Data

- Correllated and Cointegrated Pairs

- Performing OLS and Checking for Stationarity on Spread

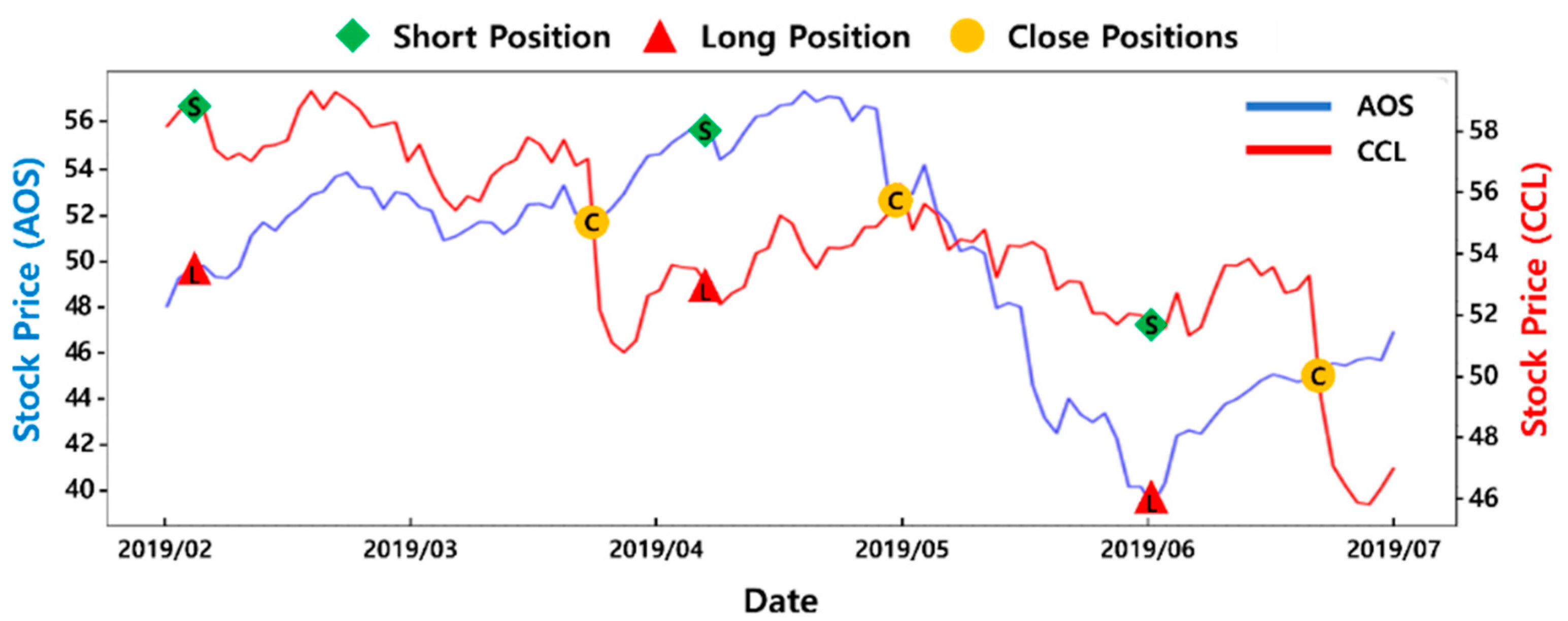

- Creating Trading Signals on Price Ratio

- Backtesting results

- Though we do have the CAGR I would like to explore and create some plots for the benchmark and cummilative returns and also look at some underwater plots.