Backtesting of a fair value gap trading strategy on a rolling 300 data point input Executable with M1-M30 timeframes, selectable exchanges and assets i.e.: python3 main.py -a 'AVAX' -t '15m' -d '2021-11-03' -e 'binance'

-

Move FVG shading anchor to start of detection date ☑

-

Filter out invalidated FVG zones at point of consumption ☑

-

Begin defining a set of entry strats depending on the last n-(10 to 20) candle movements ☑

-

Build in entry/exit position commands + fit to 1:1.5 or something ☑

-

Clean up a load of stuff for plug and play of strats, bit messy atm as i was just wanting to get soemthing working lol ☑

-

Introduce mutli-asset asyncio executions with complete PnL charting after

-

Come up with some better research into FVG delta qualifications

-

Introduce some proper risk/reward ratios

-

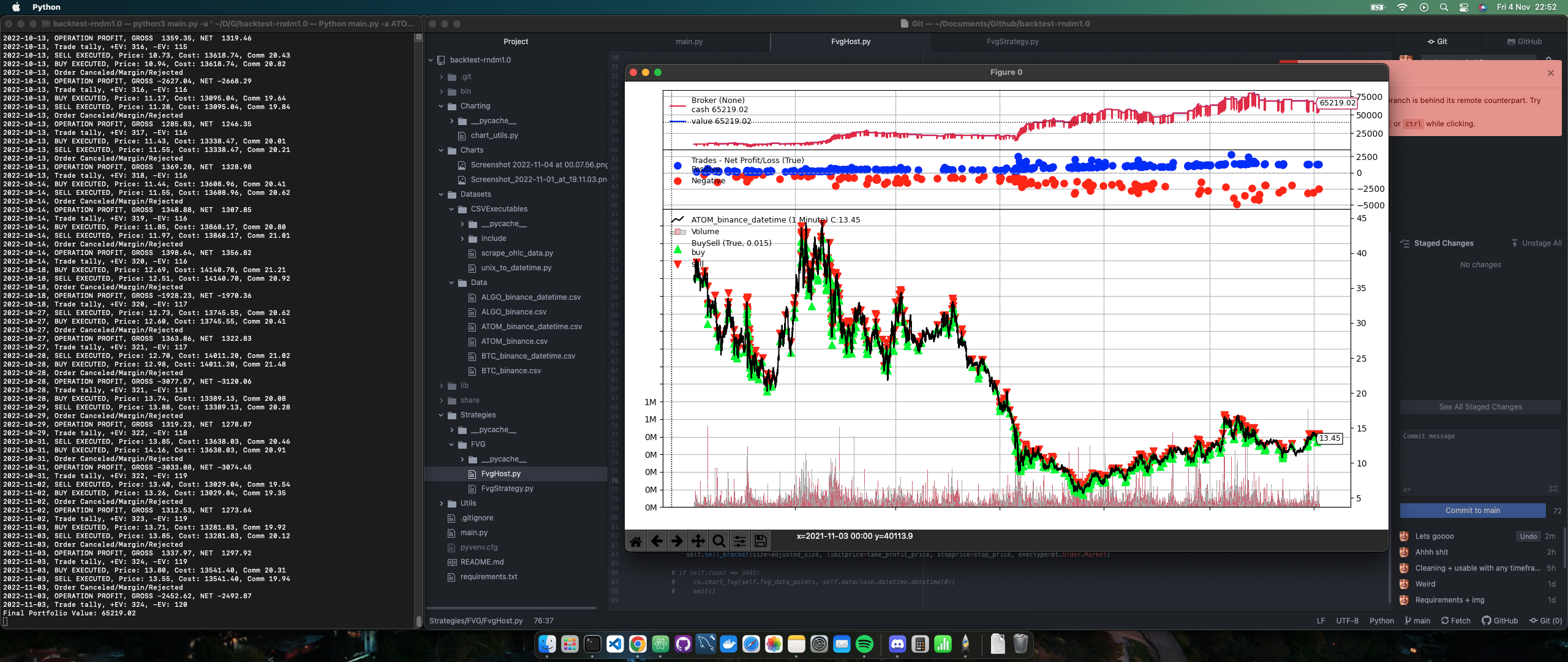

Backtested with 10x leverage and numbers are shown in the above PnL chart, cant be true surely? Got to be some fuckery going on

- ATOM - 10x Leverage - 1000USD -> 6521.90USD - M15 1 year (Trade EV, +EV: 324, -EV: 120) Config: -60 Rolling Window, 0.99/1.01, M15

- SUSHI - 10x Leverage - 1000USD -> 9044.50USD - M15 1 year (Trade EV, +EV: 373, -EV: 143) Config: -60 Rolling Window, 0.99/1.01, M15