![]()

This package contains Monte-Carlo implementations of many financial models derived from a common interface class. This interface allows for

- Shared utilities that can be used for all models for tasks such as calculating implied vol surface.

- Price Calculators that are model invariant.

- High performance, even with a large number of paths.

- New models can be created outside this repositary, by indepedent contributors, and yet be compatible with above utilities and calculators.

|

|

|

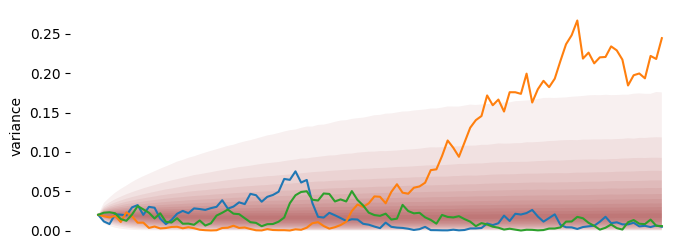

| Hull-White with a term structure of rates. | Paths of Variance in Heston Model. |

pip install finmcThis is an example of pricing a vanilla option using the local volatility model.

import numpy as np

from finmc.models.localvol import LVMC

from finmc.calc.option import opt_price_mc

# Define Dataset with zero rate curve, and forward curve.

dataset = {

"MC": {"PATHS": 100_000, "TIMESTEP": 1 / 250},

"BASE": "USD",

"ASSETS": {

"USD":("ZERO_RATES", np.array([[2.0, 0.05]])),

"SPX": ("FORWARD", np.array([[0.0, 5500], [1.0, 5600]])),

},

"LV": {"ASSET": "SPX", "VOL": 0.3},

}

model = LVMC(dataset)

price = opt_price_mc(5500.0, 1.0, "Call", "SPX", model)