Lightweight, open-source crypto portfolio optimizer.

10 optimization strategies, 8 risk metrics, AI-powered views, DeFi yields, sentiment analysis — all from a single CLI or interactive dashboard.

Installation • Who Is This For • Quick Start • Dashboard • Strategies • Features • Python API

Most portfolio optimization tools are built for equities. Crypto is different — 24/7 markets, extreme volatility, fat-tailed returns, and correlations that spike during crashes. Orbiter is built specifically for this.

- Fast — Real optimization (not brute-force), results in seconds

- Honest — Walk-forward backtesting to avoid overfitting

- Practical — CLI for quick analysis, dashboard for exploration, Python API for integration

- Comprehensive — From basic mean-variance to regime detection and factor models

You hold multiple crypto assets and want to know the optimal allocation — not just gut feeling, but mathematically optimized weights based on real risk-return tradeoffs. Orbiter tells you exactly how much to put in each coin, shows you the efficient frontier, and validates the strategy with out-of-sample backtesting so you're not just curve-fitting to the past.

What you get:

- Run

orbiter optimize BTC ETH SOL AVAXand get an allocation in seconds - See how your portfolio would have performed with walk-forward backtesting

- Understand your actual risk exposure — max drawdown, CVaR, tail risk

- Compare 7 different strategies side-by-side to find what fits your risk tolerance

You're studying portfolio theory, crypto markets, or quantitative finance and need a clean, well-tested codebase to experiment with. Every module is independent, documented, and covered by tests.

What you get:

- Factor model with market, momentum, size, and liquidity factors for crypto

- Regime detection (HMM) to study bull/bear/sideways market dynamics

- Monte Carlo stress testing with fat-tailed (Student-t) distributions

- Efficient frontier computation, correlation analysis, covariance estimation

- All code is modular — import just the pieces you need into your own research

You're building a trading system, a portfolio dashboard, or an automated rebalancing bot. Orbiter gives you a clean Python API to plug into your stack.

What you get:

pip install orbiter-cryptoand import directly — no API keys needed for price data- Programmatic access to all strategies, metrics, and stress tests

- Rebalancing simulation with transaction cost modeling (maker/taker fees, slippage)

- Calendar, threshold, or hybrid rebalancing triggers

- Works with any exchange supported by ccxt (Binance, Bybit, Kraken, OKX, etc.)

You manage crypto allocations for clients or a fund and need institutional-grade analytics without paying for Bloomberg PORT.

What you get:

- Ledoit-Wolf shrinkage covariance — the same estimator used by institutional quant desks

- Risk parity and HRP — strategies used by Bridgewater and other systematic funds

- Correlation stress testing — see how your diversification breaks down during crashes

- Factor decomposition — understand what's driving your portfolio returns

- Interactive Streamlit dashboard for client presentations and exploration

pip install orbiter-cryptoWith the interactive dashboard:

pip install orbiter-crypto[dashboard]Or install from source:

git clone https://github.com/borghei/orbiter.git

cd orbiter

pip install -e ".[dashboard]"# Find the optimal allocation for a portfolio

orbiter optimize BTC ETH SOL AVAX --strategy max-sharpe

# Try different strategies

orbiter optimize BTC ETH SOL AVAX BNB --strategy hrp

orbiter optimize BTC ETH SOL --strategy risk-parity

# Regime-aware: auto-detects bull/bear/sideways and picks the best strategy

orbiter optimize BTC ETH SOL AVAX --strategy regime-aware

# Walk-forward backtest with out-of-sample validation

orbiter backtest BTC ETH SOL AVAX --strategy hrp --train-days 180 --test-days 30

# Stress test your portfolio (Monte Carlo + correlation stress)

orbiter stress BTC ETH SOL AVAX --distribution student-t --horizon 30

# Discover top coins by market cap

orbiter discover --top 30

# Launch the interactive dashboard

orbiter dashboardStrategy: Hierarchical Risk Parity

Optimal Allocation

┏━━━━━━━┳━━━━━━━━┳━━━━━━━━━━━━━━━━━━━━━━━┓

┃ Asset ┃ Weight ┃ ┃

┡━━━━━━━╇━━━━━━━━╇━━━━━━━━━━━━━━━━━━━━━━━┩

│ BTC │ 53.3% │ █████████████████████ │

│ ETH │ 17.0% │ ██████ │

│ SOL │ 15.5% │ ██████ │

│ AVAX │ 14.2% │ █████ │

└───────┴────────┴───────────────────────┘

Portfolio Metrics

┏━━━━━━━━━━━━━━━━━┳━━━━━━━━┓

┃ Metric ┃ Value ┃

┡━━━━━━━━━━━━━━━━━╇━━━━━━━━┩

│ Ann. Return │ -18.8% │

│ Ann. Volatility │ 56.7% │

│ Sharpe Ratio │ -0.33 │

│ Sortino Ratio │ -0.46 │

│ Max Drawdown │ -58.4% │

│ Calmar Ratio │ -0.32 │

│ CVaR (95%) │ -6.72% │

│ Omega Ratio │ 0.95 │

└─────────────────┴────────┘

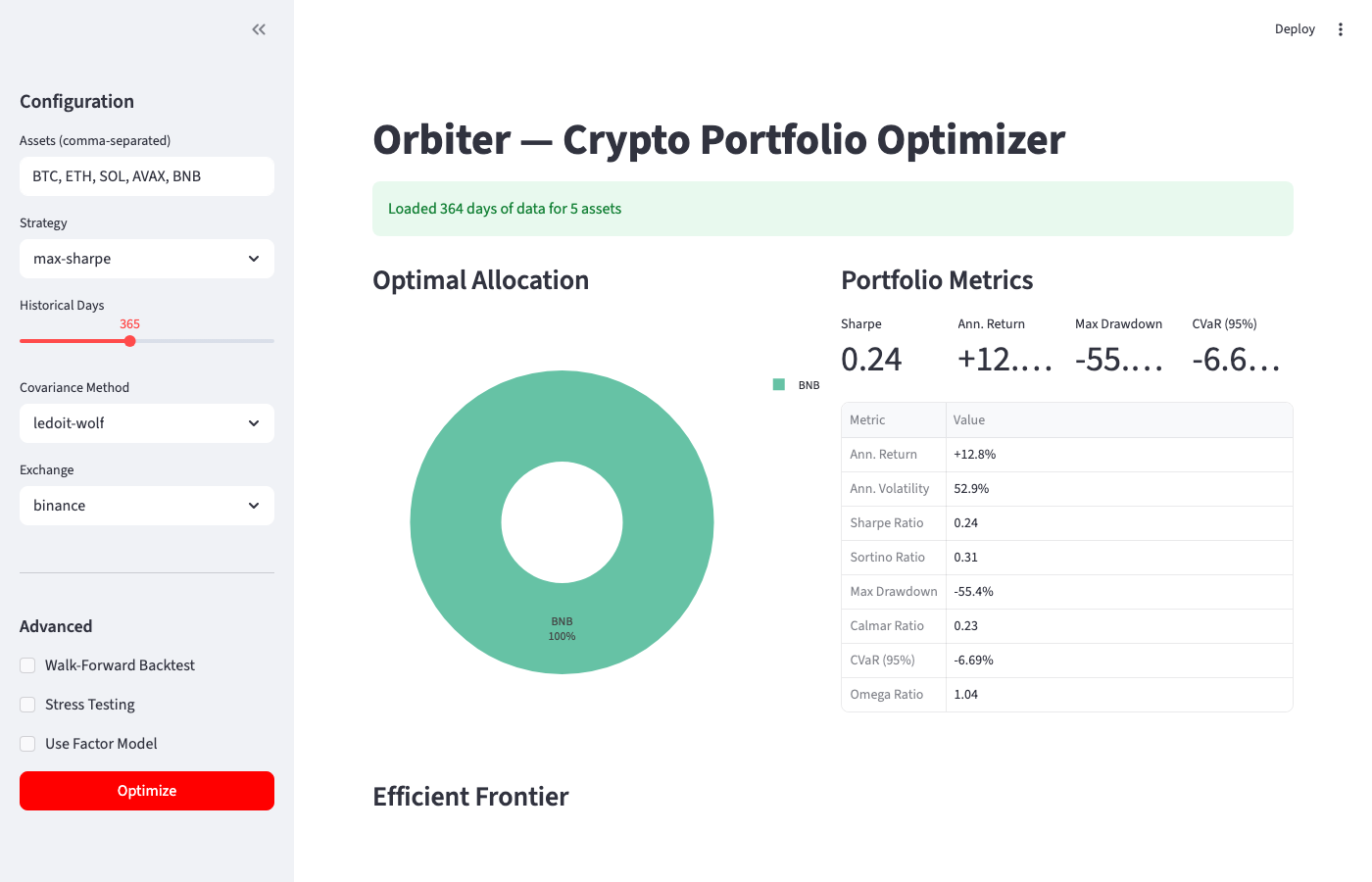

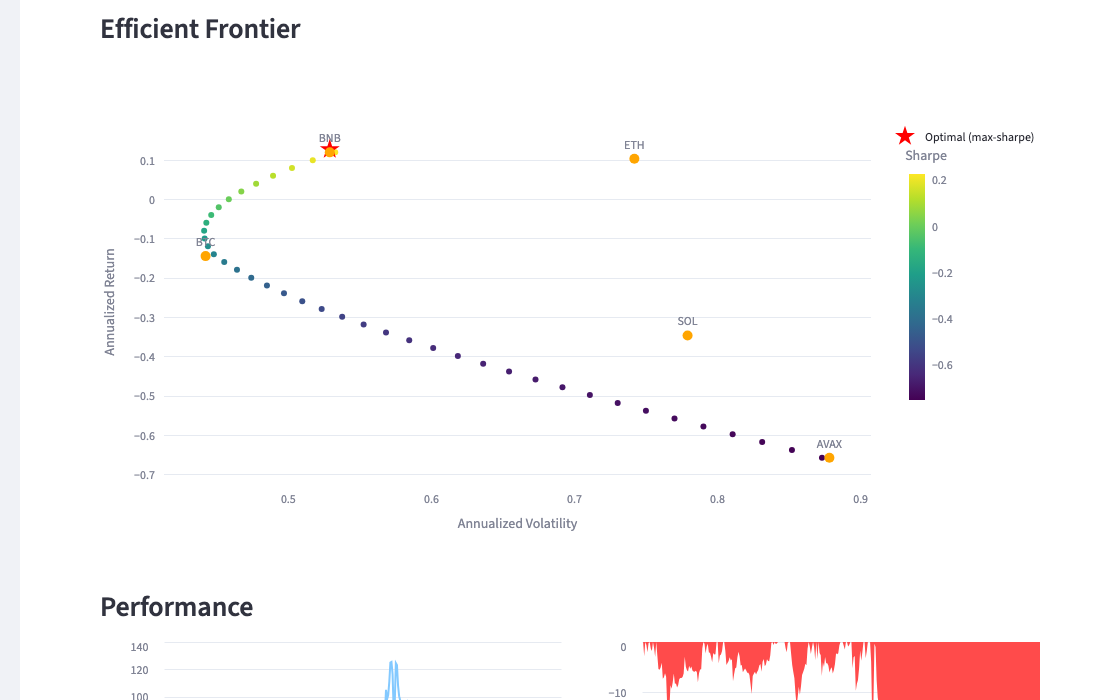

Launch with orbiter dashboard and open http://localhost:8501.

The dashboard provides:

- Sidebar configuration — pick assets, strategy, covariance method, exchange, lookback period

- Allocation pie chart — see how your portfolio is weighted

- Metrics overview — Sharpe, return, drawdown, CVaR at a glance

- Efficient frontier — interactive scatter plot showing the risk-return tradeoff

- Performance chart — cumulative returns vs equal-weight benchmark

- Drawdown chart — visualize peak-to-trough declines

- Correlation heatmap — understand how your assets move together

Toggle advanced features in the sidebar:

- Walk-Forward Backtest — out-of-sample validation with weight history

- Stress Testing — Monte Carlo VaR/CVaR + correlation stress

- Factor Model — factor loadings heatmap and R-squared per asset

| Strategy | Description | Best For |

|---|---|---|

max-sharpe |

Maximize risk-adjusted return (Sharpe ratio) | Aggressive growth |

min-vol |

Minimize portfolio volatility | Capital preservation |

min-cvar |

Minimize tail risk (Conditional Value-at-Risk) | Downside protection |

risk-parity |

Equal risk contribution from each asset | Balanced exposure |

hrp |

Hierarchical Risk Parity — correlation-based, no return estimates | Robust diversification |

regime-aware |

HMM detects bull/bear/sideways, auto-switches strategy | Adaptive allocation |

factor-max-sharpe |

Max Sharpe using factor-model implied returns | Data-driven views |

black-litterman |

Black-Litterman model with investor views (manual or AI-generated) | Subjective + quantitative |

sentiment-regime |

HMM + Fear & Greed, funding rates, exchange flows | Early regime detection |

yield-adjusted |

Max Sharpe with DeFi staking/lending yields factored in | Yield-aware allocation |

Every optimization returns 8 risk metrics:

| Metric | Description |

|---|---|

| Annualized Return | Geometric mean return, annualized to 365 days |

| Annualized Volatility | Standard deviation of returns, annualized |

| Sharpe Ratio | Return per unit of risk |

| Sortino Ratio | Return per unit of downside risk |

| Max Drawdown | Largest peak-to-trough decline |

| Calmar Ratio | Return divided by max drawdown |

| CVaR (95%) | Expected loss in the worst 5% of scenarios |

| Omega Ratio | Probability-weighted gains over losses |

| Method | Description |

|---|---|

ledoit-wolf |

Shrinkage estimator — default, most robust for small samples |

sample |

Standard sample covariance |

exponential |

Exponentially weighted — gives more weight to recent data |

Prevents overfitting by separating training and testing periods:

orbiter backtest BTC ETH SOL AVAX --strategy hrp --train-days 180 --test-days 30- Train on 180 days of data → find optimal weights

- Test those weights on the next 30 days (out-of-sample)

- Slide forward, repeat

- Report aggregated out-of-sample performance vs equal-weight benchmark

orbiter stress BTC ETH SOL AVAX --distribution student-t --horizon 30 --corr-stress 2.0- Monte Carlo simulation — 10,000 paths with normal or Student-t (fat-tailed) distributions

- VaR & CVaR — at 95% and 99% confidence levels

- Correlation stress — see how portfolio risk increases when correlations spike (as they do during crashes)

Hidden Markov Model identifies three market states:

| Regime | Characteristics | Strategy Used |

|---|---|---|

| Bull | Positive drift, moderate volatility | max-sharpe |

| Sideways | No clear direction, low volatility | risk-parity |

| Bear | Negative drift, high volatility | min-vol |

orbiter optimize BTC ETH SOL AVAX --strategy regime-awareCrypto-specific four-factor model:

- Market — overall market return (equal or cap-weighted)

- Momentum — long recent winners, short recent losers

- Size — small-cap minus large-cap returns

- Liquidity — high-volume minus low-volume returns

orbiter optimize BTC ETH SOL AVAX --strategy factor-max-sharpe --use-factorsCombine market equilibrium with your own views — or let AI generate them:

from orbiter import BlackLitterman, View, get_ai

from orbiter.prompts import MARKET_VIEWS_SYSTEM, market_views_prompt

from orbiter.black_litterman import parse_ai_views

# Manual views

views = [

View(asset="SOL", return_view=0.30, confidence=0.7),

View(asset=("ETH", "BTC"), return_view=0.05, confidence=0.6),

]

bl = BlackLitterman(returns)

result = bl.optimize(views)

# Or generate views with AI (Claude, OpenAI, or Perplexity)

ai = get_ai("claude") # reads ANTHROPIC_API_KEY from env

response = ai.generate(MARKET_VIEWS_SYSTEM, market_views_prompt(...))

views = parse_ai_views(response, assets=["BTC", "ETH", "SOL"])

result = bl.optimize(views)Supports three AI providers with a single middleware:

| Provider | Model | Env Variable |

|---|---|---|

| Claude | claude-sonnet-4-20250514 |

ANTHROPIC_API_KEY |

| OpenAI | gpt-4o |

OPENAI_API_KEY |

| Perplexity | sonar-pro |

PERPLEXITY_API_KEY |

pip install orbiter-crypto[ai] # installs anthropic + openai SDKsGoes beyond price-only HMM by fusing multiple sentiment signals:

- Fear & Greed Index — free API, updated daily

- Funding rates — crowded leverage detection from perpetual futures

- Exchange net flows — coins moving to exchanges = selling pressure

from orbiter import SentimentCollector

from orbiter.regime import SentimentRegimeModel

collector = SentimentCollector(exchange="binance")

sentiment = collector.collect(["BTC", "ETH", "SOL"])

model = SentimentRegimeModel(n_regimes=3)

model.fit(market_returns, sentiment_features_df)

regime = model.current_regime(market_returns, sentiment_features_df)Staking ETH at 3.5% APY changes the efficient frontier. Orbiter accounts for this:

from orbiter import YieldCollector

from orbiter.defi import adjust_expected_returns

yields = YieldCollector().collect(["ETH", "SOL", "ATOM"])

adjusted_mu = adjust_expected_returns(daily_returns.mean(), yields)- Pulls live yields from DeFiLlama (7000+ protocols)

- Falls back to conservative manual estimates if API is down

- Includes yield reliability scoring (higher APY = more smart contract risk)

Built-in fee and slippage models for realistic simulations:

- Maker/taker exchange fees

- Bid-ask spread costs

- Almgren-Chriss square-root market impact model

Three rebalancing triggers:

| Trigger | Description |

|---|---|

calendar |

Rebalance every N days |

threshold |

Rebalance when any weight drifts beyond a threshold |

hybrid |

Threshold check on a calendar schedule |

orbiter discover --top 20 --min-mcap 1000000000Fetches top coins from CoinGecko by market cap, with price and volume data.

from orbiter import PriceLoader, PortfolioOptimizer

loader = PriceLoader(exchange="binance")

returns = loader.get_returns(["BTC", "ETH", "SOL", "AVAX"], days=365)

optimizer = PortfolioOptimizer(returns, cov_method="ledoit-wolf")

result = optimizer.optimize("max-sharpe")

print(result.weights)

print(result.metrics)frontier = optimizer.efficient_frontier(n_points=50)

# DataFrame with columns: return, volatility, sharpe, BTC, ETH, SOL, AVAXfrom orbiter.backtest import WalkForwardBacktest

bt = WalkForwardBacktest(returns, train_days=180, test_days=30, strategy="hrp")

result = bt.run()

print(result.metrics) # Out-of-sample performance

print(result.weights_history) # Weights at each rebalancefrom orbiter.stress import monte_carlo_stress, correlation_stress

# Monte Carlo with fat tails

mc = monte_carlo_stress(

weights=result.weights.values,

mu=returns.mean().values,

cov=returns.cov().values,

distribution="student-t",

df=5.0,

horizon_days=30,

)

print(mc["cvar_95"], mc["var_99"])

# Correlation stress

cs = correlation_stress(weights, cov_matrix, stress_factor=2.0)

print(cs["stressed_volatility"])from orbiter.factors import CryptoFactorModel

model = CryptoFactorModel(returns)

exposures = model.fit()

print(exposures.loadings) # Factor betas per asset

print(exposures.r_squared) # Model fit per asset

print(model.expected_returns()) # Factor-implied expected returnsfrom orbiter.regime import RegimeModel

model = RegimeModel(n_regimes=3)

model.fit(returns["BTC"])

regime = model.current_regime(returns["BTC"])

print(regime) # Regime.BULL, Regime.SIDEWAYS, or Regime.BEAR

print(model.get_strategy(regime))from orbiter.rebalance import simulate_rebalancing, RebalanceConfig, RebalanceTrigger

from orbiter.costs import FeeSchedule

config = RebalanceConfig(

trigger=RebalanceTrigger.THRESHOLD,

drift_threshold=0.05,

fee_schedule=FeeSchedule(maker=0.001, taker=0.001),

)

result = simulate_rebalancing(returns, target_weights, config)

print(result.total_turnover)

print(result.total_cost)

print(result.metrics)| Source | Data | API Key |

|---|---|---|

| Binance (via ccxt) | OHLCV price data | Not required |

| Any ccxt exchange | OHLCV price data | Not required |

| CoinGecko | Market caps, coin discovery | Not required (free tier) |

| Blockchain.com | BTC active addresses, NVT ratio | Not required |

Change the exchange:

orbiter optimize BTC ETH SOL --exchange kraken

orbiter optimize BTC ETH SOL --exchange bybit| Command | Description |

|---|---|

orbiter optimize SYMBOLS... |

Optimize portfolio allocation |

orbiter backtest SYMBOLS... |

Walk-forward backtest |

orbiter stress SYMBOLS... |

Monte Carlo + correlation stress test |

orbiter discover |

List top coins by market cap |

orbiter dashboard |

Launch Streamlit dashboard |

Run orbiter COMMAND --help for full options.

src/orbiter/

├── data.py # Price fetching via ccxt

├── data_sources.py # CoinGecko, on-chain metrics

├── metrics.py # Risk & performance metrics

├── covariance.py # Covariance estimation (sample, Ledoit-Wolf, exponential)

├── optimize.py # 10 optimization strategies + efficient frontier

├── backtest.py # Walk-forward backtesting engine

├── costs.py # Transaction cost & slippage modeling

├── rebalance.py # Rebalancing simulation (calendar/threshold/hybrid)

├── regime.py # HMM regime detection + sentiment-enhanced regime

├── stress.py # Monte Carlo & correlation stress testing

├── factors.py # Crypto factor model (market, momentum, size, liquidity)

├── black_litterman.py # Black-Litterman model with AI-generated views

├── ai.py # AI middleware (Claude, OpenAI, Perplexity adapters)

├── prompts.py # Prompt templates for AI-powered analysis

├── sentiment.py # Fear & Greed, funding rates, exchange flows

├── defi.py # DeFi yield data from DeFiLlama

├── cli.py # Click CLI

└── dashboard.py # Streamlit interactive dashboard

MIT + Commons Clause — Free to use in open-source projects, personal use, education, and internal business workflows. You cannot sell this software or repackage it as a paid product. See LICENSE for full terms.