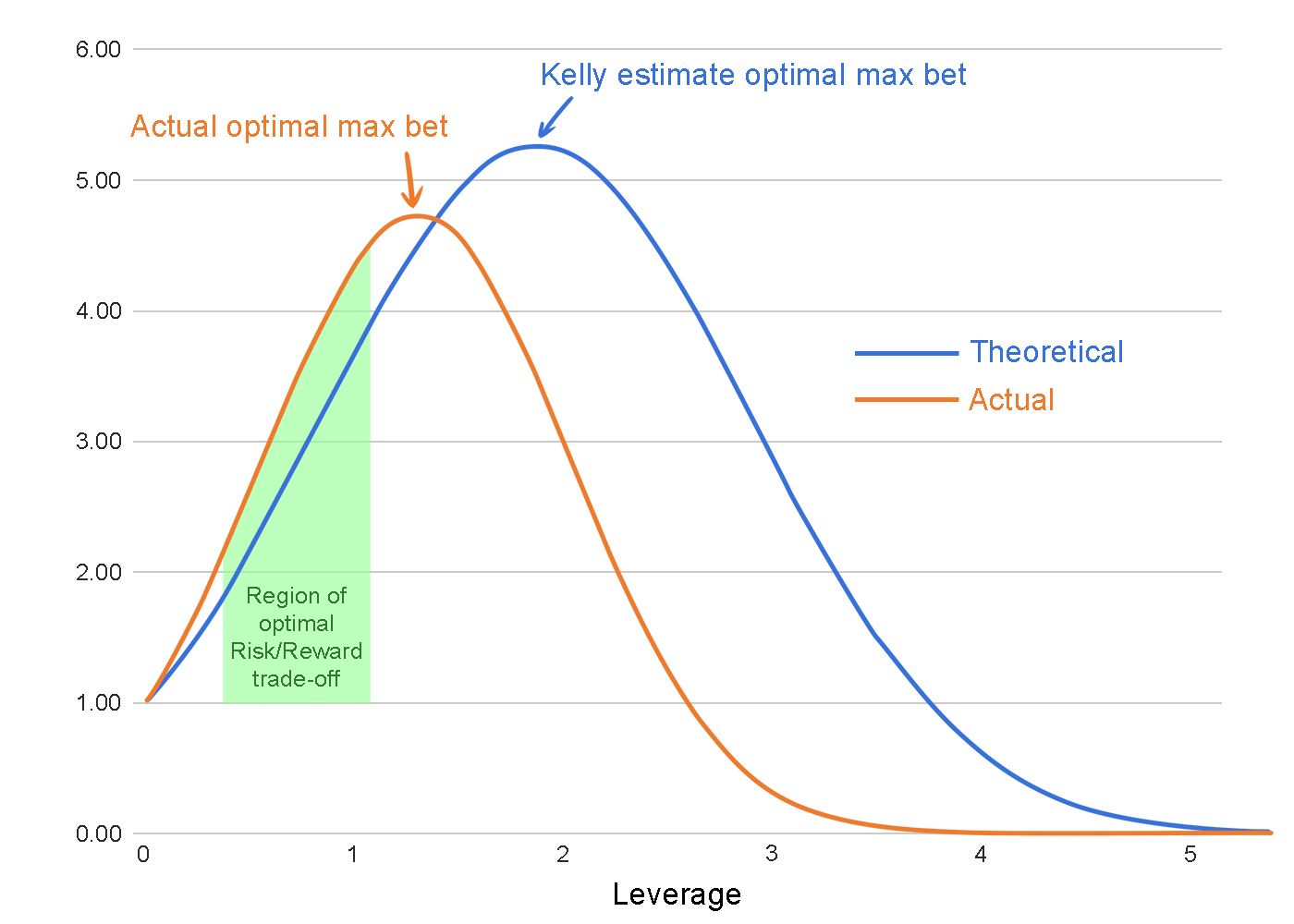

Based on: Kelly, J. L., Jr. (1956). "A New Interpretation of Information Rate." Bell System Technical Journal, 35(4), 917–926. doi:10.1002/j.1538-7305.1956.tb03809.x

A stupidly fast, native C++ Python extension implementing the Kelly Criterion for optimal bet (but lets call them 'investments' instead) sizing.

pip install kelzerimport kelzerReturns the optimal fraction of bankroll to wager.

| Parameter | Type | Required | Default | Description |

|---|---|---|---|---|

win_prob |

float | yes | — | Probability of winning, in (0, 1) |

decimal_odds |

float | yes | — | Decimal odds, must be > 1 |

multiplier |

float | no | 1.0 | Fraction of Kelly to apply, in (0, 1] |

decimals |

int | no | 4 | Decimal places to round result to (0–15) |

import kelzer

# Full Kelly — 60% chance at 2.0 odds

kelzer.fraction(0.6, 2.0)

# 0.2

# Quarter Kelly

kelzer.fraction(0.6, 2.0, multiplier=0.25)

# 0.05

# Half Kelly, 6 decimal places

kelzer.fraction(0.55, 1.9, multiplier=0.5, decimals=6)

# 0.055556

# Negative edge — don't bet

kelzer.fraction(0.3, 2.0)

# -0.4kelzer.fraction(0.0, 2.0) # ValueError: win_prob must be in (0, 1)

kelzer.fraction(0.6, 1.0) # ValueError: decimal_odds must be > 1

kelzer.fraction(0.6, 2.0, multiplier=0.0) # ValueError: multiplier must be in (0, 1]f* = (b·p − q) / b

Where b = decimal_odds − 1, p = win_prob, q = 1 − p. The result is then scaled by multiplier.

Apache 2.0