Wrong-Way Risk (WWR) estimation for counterparty credit risk.

📖 Documentation · 🎮 Live playground · 📊 Worked example · 📄 Paper (PDF)

wayfault quantifies the adverse dependence between exposure and counterparty

credit quality — the risk that exposure rises precisely when the counterparty

deteriorates (WWR), and its favourable mirror, Right-Way Risk (RWR). It takes a

Monte-Carlo exposure cube and a credit curve as inputs and produces:

- baseline (independence-assumption) exposure metrics and CVA,

- a conditional expected exposure given default under a pluggable dependence model,

- a WWR-adjusted CVA and the empirical alpha multiplier

α = WWR-CVA / independent-CVA, - ML-based calibration of the dependence parameter,

- WWR/RWR classification and diagnostics.

The library does not generate exposures or bootstrap curves — those are inputs.

An interactive browser playground

runs the real wayfault wheel via WebAssembly (Pyodide) — no install, no server.

Adjust the dependence model and parameters and watch the CVA, alpha multiplier,

and exposure charts recompute live.

wayfault follows a strict hexagonal (ports & adapters) design. The

dependency rule points inward: adapters → application → ports → domain. The

domain, application, and ports layers import only the standard library

and numpy. Optional adapters import their heavy dependencies lazily and

raise a clear MissingDependencyError if the extra is not installed.

pip install wayfault # core (numpy only)

pip install 'wayfault[io,ml,viz]' # with optional extrasFor local development (editable install with the dev tooling):

pip install -e '.[io,ml,viz,dev]'Optional extras:

| Extra | Enables | Pulls in |

|---|---|---|

[io] |

CSV/Parquet source adapters | pandas, pyarrow |

[ml] |

scikit-learn survival calibrator | scikit-learn |

[viz] |

diagnostic plots | matplotlib |

[dev] |

tests, type-checking, linting | pytest, mypy, … |

import numpy as np

from wayfault import estimate_wwr

from wayfault.adapters.outbound.exposure_inmemory import InMemoryExposureSource

from wayfault.adapters.outbound.credit_flat import FlatHazardCreditCurveSource

from wayfault.adapters.outbound.dependence_hullwhite import HullWhiteHazardModel

cube = np.random.default_rng(0).normal(size=(10_000, 12)) + 1.0 # scenarios x tenors

tenors = [i / 4 for i in range(1, 13)] # quarterly to 3y

result = estimate_wwr(

exposure=InMemoryExposureSource(cube, tenors),

credit=FlatHazardCreditCurveSource(hazard=0.02, recovery=0.4),

model=HullWhiteHazardModel(b=0.5), # b > 0 -> wrong-way

)

print(result.baseline_cva, result.wwr_cva, result.alpha, result.classification)A full runnable example lives in

examples/quickstart.py

and uses only the in-memory adapters (zero extras).

python -m wayfault estimate \

--exposure cube.csv --credit curve.csv \

--model hullwhite --b 0.5 --out result.json(--exposure/--credit CSV ingestion requires the [io] extra.)

| Model | Knob | WWR when | Notes |

|---|---|---|---|

IndependentModel |

— | — | conditional EE ≡ unconditional EE |

HullWhiteHazardModel |

b |

b > 0 |

λ(t) = exp(a(t) + b·V(t)) (Hull–White) |

GaussianCopulaModel |

ρ |

ρ > 0 |

one-factor Gaussian copula |

ClaytonCopulaModel |

θ |

θ > 0 |

Archimedean, lower-tail dependence |

FrankCopulaModel |

θ |

θ > 0 |

Archimedean, symmetric (sign sets direction) |

All models are numpy-only and fully vectorised across tenors.

RegressionCalibrator— numpy-only OLS estimate of the Hull–Whiteb.SklearnSurvivalCalibrator—[ml]covariate-hazard surrogate.

Invert the relationship — target-driven calibration and reverse-stress:

from wayfault import calibrate_to_alpha, find_breakpoint

hw = lambda b: HullWhiteHazardModel(b=b)

calibrate_to_alpha(exposure, credit, hw, target_alpha=1.25, lo=-1.5, hi=1.5) # which b -> alpha 1.25?

find_breakpoint(exposure, credit, hw, threshold=1.40, lo=0.0, hi=3.0) # b where alpha breaches 1.40The [viz] extra adds a beautiful matplotlib plotting module

(wayfault.adapters.outbound.viz) — lazily imported, so the core stays

numpy-only. Regenerate the gallery with pip install 'wayfault[viz]' then

python examples/gallery.py.

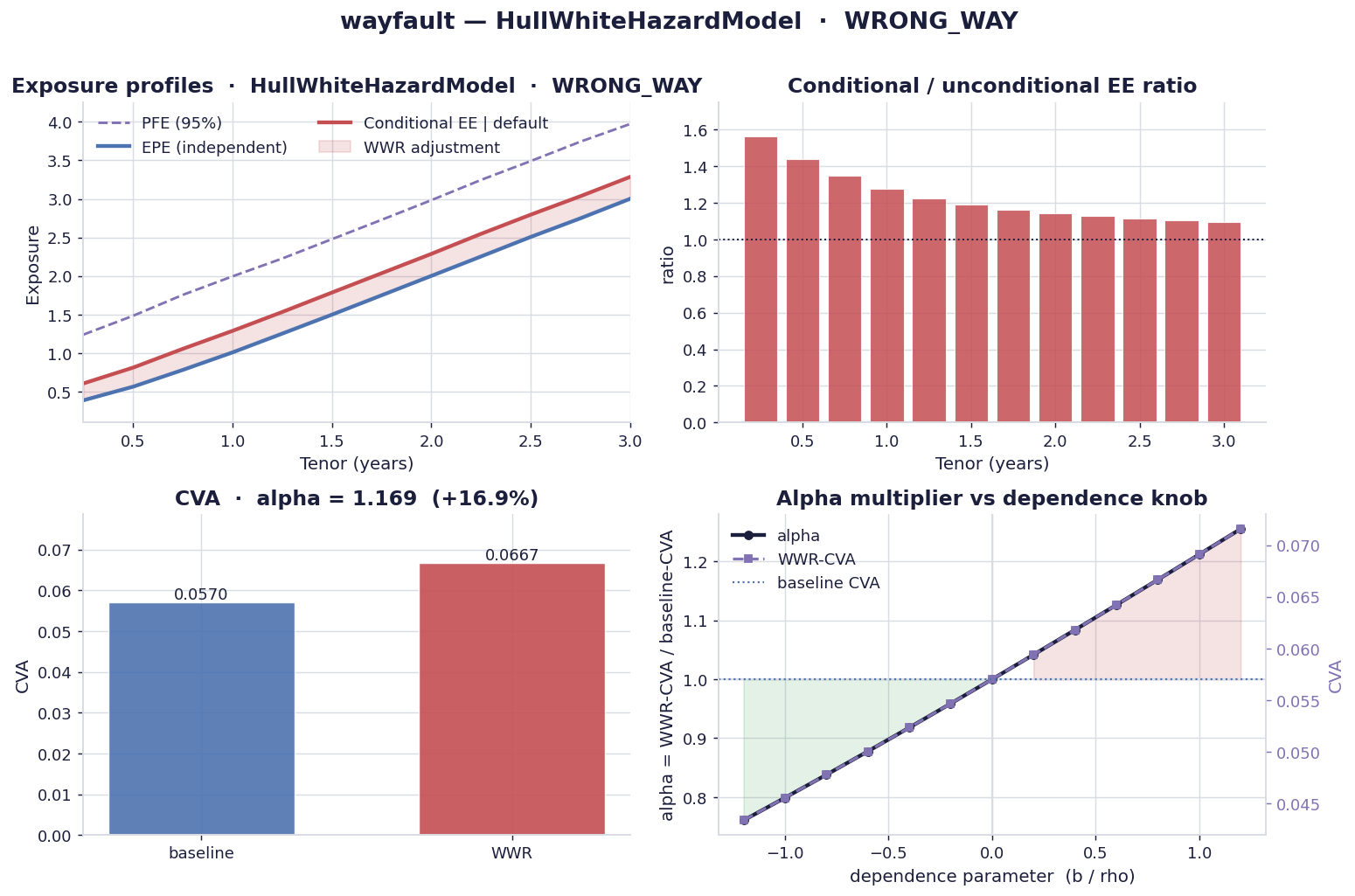

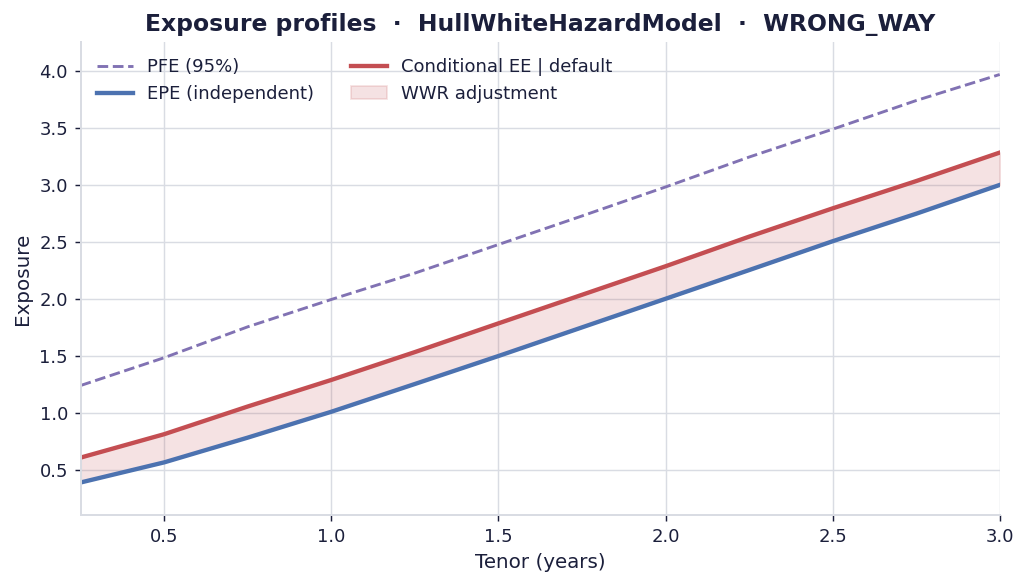

| Exposure profiles — EPE vs conditional EE, shaded WWR adjustment | EE ratio — per-tenor conditional/unconditional |

|

|

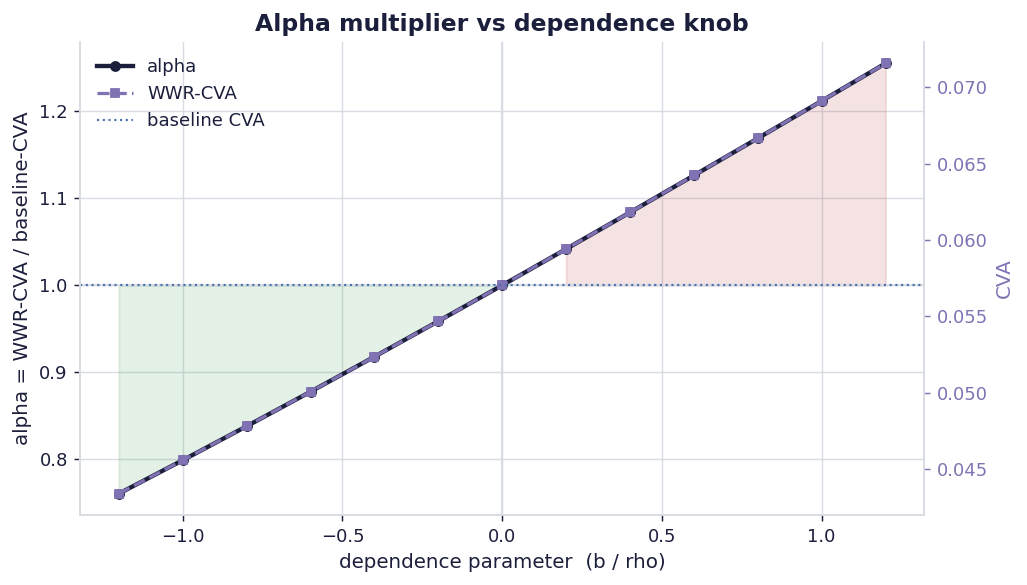

| Alpha sweep — alpha & CVA vs the dependence knob | Dashboard — everything at a glance |

|

|

from wayfault.adapters.outbound import viz

fig = viz.plot_dashboard(result, bs=bs, alphas=alphas, wwr_cvas=wwr_cvas)

viz.save(fig, "dashboard.png")Two acceleration techniques, both numpy-only:

- Vectorised re-weighting — every model re-weights the whole exposure cube in a single numpy expression (no per-tenor Python loop).

- Parallel batch & sweep —

wayfault.application.parallelfans independent estimates across workers with deterministic, input-order results:

from wayfault.application.parallel import sweep_models

from wayfault.adapters.outbound.dependence_hullwhite import HullWhiteHazardModel

results = sweep_models(

exposure, credit,

[HullWhiteHazardModel(b=b) for b in np.linspace(-1.2, 1.2, 25)],

max_workers=8, # threads (numpy releases the GIL); or pass a ProcessPoolExecutor

)

alphas = [r.alpha for r in results]See the Performance docs.

pytest # tests

mypy --strict src # type checks

ruff check # lintReference: Hull & White, CVA and Wrong-Way Risk (2012).

MIT.